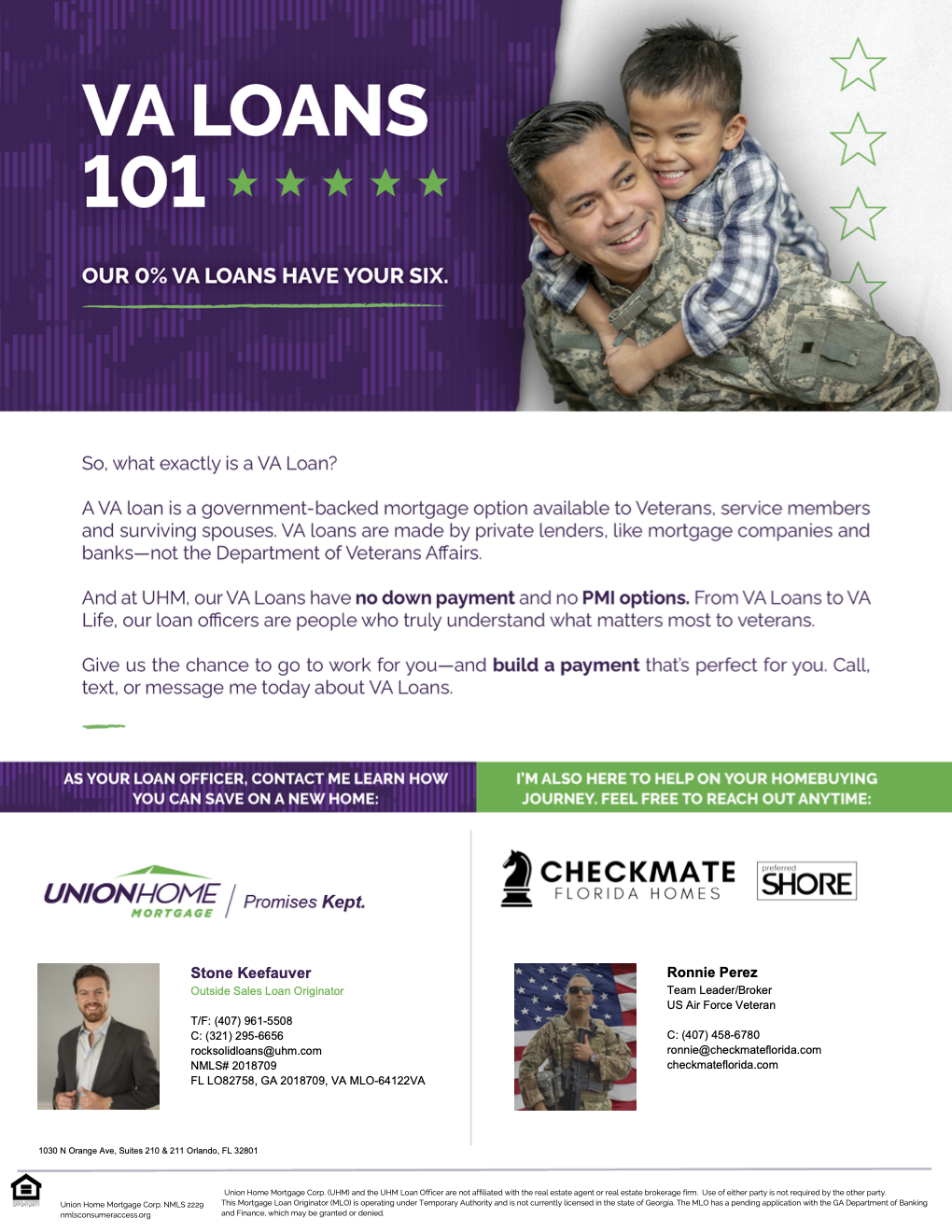

SERVING OUR VETERANS

FLORIDA HAS UNIQUE PROGRAMS FOR VETERAN FLORIDA BUYERS

FLORIDA HOMETOWN HERO - CHRISTIAN IRIAS - 0% DOWNPAYMENT HOME SALE WITH VA LOAN

-

0% DOWN PAYMENT

No down payment as long as the sales price is at or below the home’s appraised value (the value set for the home after an expert review of the property).

-

NO LOAN LIMIT

No loan limit with full entitlement if you can afford the loan, VA will back loans in all areas of the country, regardless of home price.

-

COMPETITIVE TERMS AND RATES

Competitive terms and interest rates from private banks, mortgage lenders, or credit unions.

-

NO PMI

PMI is a type of insurance that protects the lender if the borrower ends up not being able to pay the mortgage. It’s usually required on conventional loans if the down payment is less than 20% of the total mortgage amount.

-

LESS FEES

Fewer closing costs, which may be paid by the seller, lender, or any other party. Not having to pay PMI could save a borrower on their monthly mortgage payment.

-

NO PRE-PAY PENALTY

No penalty fee for paying off the loan early.

STEP 1

Apply for your VA home loan Certificate of Eligibility (COE) – The COE verifies to your lender that you qualify for the VA home loan benefit. If you have used your loan benefit in the past, a current COE may be helpful to know how much remaining entitlement you have or to ensure your entitlement was restored for previous VA-backed loans that were paid in full.

STEP 3

Choose a lender – You can go through a private bank, mortgage company, or credit union to get your loan. Lenders offer different loan interest rates and fees, so shop around for the loan that best meets your needs.

STEP 5

Read all agreements—and make sure you understand any charges, fees, and commissions—before signing with an agent. Remember they work for you and should put your interests first.

STEP 2

Look at your current finances – Review your credit profile, income, expenses, and monthly budget to make sure you’re ready to buy a home. Decide how much you want to spend on a mortgage—and be sure to include closing costs in the overall price. Get more advice from the Consumer Financial Protection Bureau.

STEP 4

Choose a real estate agent – Meet with one of our real estate agents and then select one to represent you in the homebuying process. You can take your lender’s pre-approval letter to your real estate agent and begin shopping.

STEP 6

Shop for a home – Look at houses in your price range until you find one that works for you.